CATEGORIES:

BiologyChemistryConstructionCultureEcologyEconomyElectronicsFinanceGeographyHistoryInformaticsLawMathematicsMechanicsMedicineOtherPedagogyPhilosophyPhysicsPolicyPsychologySociologySportTourism

The Long-Run Average Cost Curve

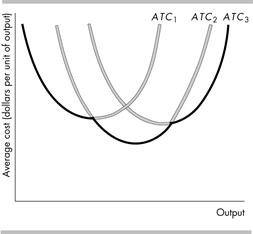

· The long-run average cost curve, LRAC, is the relationship between the lowest attainable average total cost and output when both the plant size and labor are varied. This curve is derived from the short-run average total cost curves. It shows the lowest average total cost to produce a given level of output. In the figure, the LRAC curve is the darkened parts of the three short-run ATC curves.

50. Production Function

The production function determines the behavior of long run costs.

A firm’s production function typically exhibits diminishing returns to capital as well as diminishing returns to labor. The marginal product of capital is the change in total product divided by the change in capital when the quantity of labor is held constant. Holding constant the quantity of employment, after some level of output the firm will have diminishing returns to capital—the marginal product of capital decreases as more capital is used.

Short-Run Cost and Long-Run Cost

Short-Run Cost and Long-Run Cost

In the long run, a firm can use different plant sizes. Each plant size has a different short-run ATC curve. Each short-run ATC curve is U-shaped and the larger the plant size, the greater is the output at which the average total cost is a minimum.

The figure illustrates three average total cost curves for three plant sizes. ATC1 pertains to the smallest plant size and ATC3 to the largest.

The Long-Run Average Cost Curve

The long-run average cost curve, LRAC, is the relationship between the lowest attainable average total cost and output when both the plant size and labor are varied. This curve is derived from the short-run average total cost curves. It shows the lowest average total cost to produce a given level of output. In the figure, the LRAC curve is the darkened parts of the three short-run ATC curves.

51. Economies and Diseconomies of Scale

· Economies of scale are features of a firm’s technology that lead to falling long-run average cost as output increases. With given factor prices, economies of scale occur if the percentage increase in output exceeds the percentage increase in all factors of production. The long-run average cost curve slopes downward in this range of output. The main source of economies of scale is greater specialization of both labor and capital.

· Constant returns to scale are features of a firm’s technology that lead to constant long-run average cost as output increases. With given factor prices, economies of scale occur if the percentage increase in output equals the percentage increase in all factors of production. The long run average cost curve is horizontal in this range of output.

· Diseconomies of scale are features of a firm’s technology that lead to rising long-run average cost as output increases. With given factor prices, economies of scale occur if the percentage increase in output is less than the percentage increase in all factors of production. The long run average cost curve slopes upward in this range of output.

· The minimum efficient scale is the smallest quantity of output at which the long-run average cost curve reaches its lowest level.

52. Perfect competition

· Firms in perfect competition face the maximum amount of competition because there are many competing firms, each of which produces an identical product.

· Firms in perfect competition maximize their profit by producing where MR = MC.

· Perfect competition leads to an efficient allocation of resources.

What is Perfect Competition?

Perfect competition is an industry in which

· Many firms sell identical products to many buyers

· There are no restrictions on entry into the industry

· Established firms have no advantage over existing ones

· Sellers and buyers are well informed about prices

These characteristics of perfect competition arise when the minimum efficient scale for a firm is small relative to the size of the entire market.

· Firms operating in perfect competition seek to maximize economic profit, which is the difference between total revenue (the price of the firm’s output multiplied by the quantity sold) and its total opportunity cost of production.

· Firms in perfect competition are price takers,meaning that a firm that cannot influence the market price and so it sets its own price equal to the market price.

· Because the firm is a price taker, its marginal revenue—which is the change in total revenue that results in a one-unit increase in the quantity sold—is equal to the market price and remains constant as output sold increases. The firm’s demand is perfectly elastic and the firm’s demand curve is a horizontal line at the market price.

53. The Firm’s Output Decision

Analysis and the Supply Decision

· The firm produces the quantity of output for which the difference between total revenue and total cost is at its maximum because this difference is its economic profit.

· Marginal analysis can be used to determine the profit maximizing quantity. The firm compares the marginal revenue (which remains constant with output) to the marginal cost (which changes with output) of producing different levels of output.

· When MR > MC, then the extra revenue from selling one more unit exceeds the extra cost of producing one more unit, so the firm increases its output to increase its profit.

· When MR < MC, then the extra cost of producing one more unit exceeds the extra revenue from selling one more unit, so the firm decreases its output to increase its profits

· When MR = MC, then the extra cost of producing one more unit equals the extra revenue from selling one more unit, so the firm’s profit is maximized at this level of output.

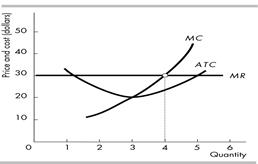

·  In the figure the firm produces 4 units of output because that is the quantity that sets the firm’s marginal cost equal to its marginal revenue, that is, MR = MC. The firm then charges the going market price of $30 for its product.

In the figure the firm produces 4 units of output because that is the quantity that sets the firm’s marginal cost equal to its marginal revenue, that is, MR = MC. The firm then charges the going market price of $30 for its product.

Temporary Shutdown Decision

· The firm will temporarily shut down in the short run when price falls below the shutdown point, which is the output and price that just allows the firm to cover its total variable cost. The minimum AVC is the lowest price at which the firm will operate because if it operated with a lower price, the firm’s loss would be greater than if it shut down. (The loss when the firm shuts down is equal to its fixed cost.)

· The firm will continue operating in the short run even if it incurs an economic loss as long as the price exceeds the minimum AVC.

The Firm’s Supply Curve

· As long as the firm remains open, it produces where MR = MC. So the firm’s supply curve is its MC curve above the minimum AVC. At prices below the minimum AVC, the firm shuts down and supplies zero.

· The figure shows the firm’s supply curve as the heavy dark line.

· At prices less than the minimum average variable cost, which equals P in the figure, the firm shuts down and supplies zero.

· At prices greater than the minimum average variable cost, the firm supplies along its marginal cost curve. Hence the firm’s marginal cost curve is its supply, indicated in the figure by the S = MC curve.

54. Output, Price, and Profit in the Short Run

The short-run market supply curve shows the quantity supplied by all the firms in the market at each price when each firm’s plant and number of firms remain the same. The quantity supplied in the industry at any price is the summation of all quantities supplied by each firm at that price, so the short-run industry supply curve is the horizontal summation of all the firms’ supply curves.

Changes in market demand influence the output and the entry or exit decisions made by firms. An increase in market demand shifts the demand curve rightward and raises the market price. Each firm in the industry responds by increasing its quantity supplied.

The higher price now exceeds each firm’s minimum ATC and the firms in the industry earn an economic profit. The figure illustrates a perfectly competitive firm earning an economic profit. The firm’s economic profit is equal to the area of the darkened rectangle.

In the short run there are three possible profit outcomes—an economic profit, zero economic profit, and an economic loss.

If the price exceeds the ATC, the firm earns an economic profit (as illustrated in the figure).

If the price equals the ATC, the firm “breaks even” by earning zero economic profit. In this case, the firm earns a normal profit. At the profit maximizing level of output, q, the price, P, equals the ATC. If the price is less than the ATC, the firm incurs an economic loss.

55. Output, Price, and Profit in the Long Run

Economic profit motivates firms to enter the industry, thereby increasing the market supply.

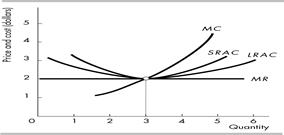

When the market supply curve shifts rightward, the market price falls. Eventually the price falls to equal the minimum ATC for each firm in the industry and firms have adjusted their plant size so they are producing at the minimum long-run average cost. At this price, firms in the industry no longer earn an economic profit and so firms no longer enter the industry. The figure illustrates this long-run equilibrium. In the figure, LRAC is the long-run average cost curve and SRAC is the short-run average cost curve.

One difference between the old and new market equilibriums is that the number of firms in the industry has risen and total quantity produced in the industry has increased.

The effects of a decrease in market demand are the opposite of those outlined above.

In the long run, competitive firms earn zero economic profit (price = average total cost).

56. Changing Tastes and Advancing Technology

57. Competition and Efficiency

Efficient Use of Resources

· Resource allocation in a market is efficient when society values no other use of the resources more highly. Resource use is efficient when production is such that the marginal social benefit of the good equals the marginal social cost of the good.

Choices, Equilibrium, and Efficiency

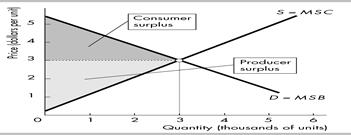

· Consumers allocate their budgets to get the most value out of them. Because consumers get the most value out of their budget, a consumer’s individual demand curve for a good is the consumer’s marginal benefit curve for the good. If no one else benefits from the good other than the consumers, then as shown in the figure the market demand curve for a good is the marginal social benefit curve.

· Firms maximize their profits in order to get the most value out of their resources. Firms make choices across all possible allocations of their resources. A firm’s supply curve for a good is its marginal cost curve. If all the costs of production of the good are paid by the producers, then as shown in the figure the market supply curve for a good is the marginal social cost curve.

·  In a competitive equilibrium, the quantity demanded equals the quantity supplied. If there are no externalities, the demand curve is the same as the marginal social benefit curve and the supply curve is the same as the marginal social cost curve, so at the competitive equilibrium, the marginal social benefit equals the marginal social cost. Resource use is efficient. Because resources are used efficiently, at the competitive equilibrium there is no other allocation of resources that will generate greater net benefits to society. The figure shows this outcome, where resource use is efficient at the equilibrium quantity of 3,000 units.

In a competitive equilibrium, the quantity demanded equals the quantity supplied. If there are no externalities, the demand curve is the same as the marginal social benefit curve and the supply curve is the same as the marginal social cost curve, so at the competitive equilibrium, the marginal social benefit equals the marginal social cost. Resource use is efficient. Because resources are used efficiently, at the competitive equilibrium there is no other allocation of resources that will generate greater net benefits to society. The figure shows this outcome, where resource use is efficient at the equilibrium quantity of 3,000 units.

58. Monopoly and How It Arises

A monopoly is a firm that produces a good or service for which no close substitute exists and which is protected by a barrier that prevents other firms from selling that good or service. A monopoly has two key features:

A monopoly is a firm that produces a good or service for which no close substitute exists and which is protected by a barrier that prevents other firms from selling that good or service. A monopoly has two key features:

· No Close Substitutes: There are no close substitutes for the good or service.

· Barriers to Entry: A constraint that protects a firm from potential competition is called a barrier to entry. Monopolies are protected by barriers to entry.

· Natural barriers to entry create a natural monopoly, which is an industry in which economies of scale enable one firm to supply the entire market at the lowest possible cost.

· An ownership barrier to entry occurs if one firm owns a significant portion of a key resource.

· Legal barriers to entry create a legal monopoly,which is a market in which competition and entry are restricted by the granting of a public franchise (an exclusive right is granted to a firm to supply a good or service—the U.S. Postal Service has a public franchise to deliver first-class mail), a government license (when the government controls entry into particular occupations, professions and industries—a license is required to practice law), a patent (an exclusive right granted to the inventor of a product or service) or a copyright (exclusive right granted to the author or composer of a literary, musical, dramatic, or artistic work).

59. Monopoly Price-Setting Strategies

A single-price monopoly is a firm that sells each unit of its output for the same price to all its customers.

Price discrimination is the practice of selling different units of a good or service for different prices. Many firms price discriminate, but not all of them are monopoly firms.

Date: 2015-12-11; view: 1998

| <== previous page | | | next page ==> |

| Marginal Cost and Average Costs | | | Unit 1 and Unit 2 Review Materials |