CATEGORIES:

BiologyChemistryConstructionCultureEcologyEconomyElectronicsFinanceGeographyHistoryInformaticsLawMathematicsMechanicsMedicineOtherPedagogyPhilosophyPhysicsPolicyPsychologySociologySportTourism

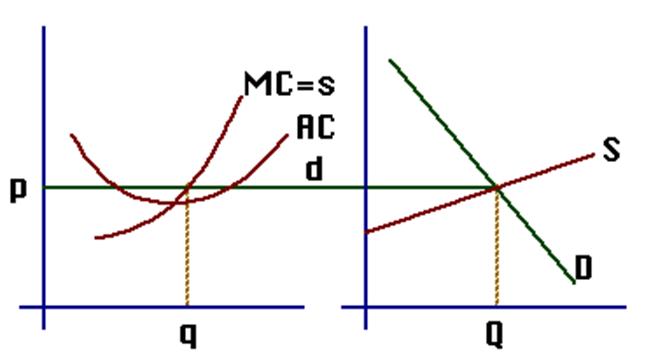

The Competitive Firm and Industry Demand

The individual firm's demand curve is different from that of the industry, and is more elastic. This is because substitutes increase elasticity, and the customer of the firm has many good substitutes for that firm's output – namely, the output of other firms in the industry. As we mentioned above, the demand curve for a P-Competitive firm is infinitely elastic:

In the figure, the lower case q, s and d refer to output, supply and demand from the point of view of the individual firm, respectively, and the capital S, D, and Q are for the industry as a whole.

49.Economic strategies of the firm in P-competitive  market

market

How much output should firm sell, at the given price to maximize profits.The answer is: increase output until P=MR=MC

How much output should firm sell, at the given price to maximize profits.The answer is: increase output until P=MR=MC

Now we will use this rule as a basic rule to consider the firm economic strategies.

In the picture just shown, the firm is making an "economic profit." All costs, explicit and implicit, are included in the firm's Average Cost curve.

Profitableness and losses conditions for perfect competitor according to MRMC-model:

a) a firm has profit under:

б) break-even condition is:

в) losses minimization condition through production continuance:

г)losses minimization condition through temporary dissolution of the firm:

г)losses minimization condition through temporary dissolution of the firm:

In other words if the cost of and additional unit (MC) is less than the revenue obtained from that same additional unit (MR), producing the additional units will add to profits (or reduce losses). If the cost of additional units of output (MC) cost more than they add to revenue (MR), the firm should not produce the additional units. The rules for profit maximization are simple:

• MR >MC – produce it!

• MR < MC – don’t produce it!

• When MR = MC – you are earning maximum profits!

MR=MC is the main principle of supply for the individual firm. Supply is the relation between the price and the quantity that people want to sell. For an individual firm, that is: the relation between the price and the quantity the firm wants to sell. So we ask: at a given price, how much will a (profit- maximizing) firm want to sell? The answer: enough so that the price is equal to marginal cost. In other words, the marginal cost curve is the supply curve for the individual firm.

Date: 2016-03-03; view: 1159

| <== previous page | | | next page ==> |

| Different market forms | | | Long run equilibrium |