CATEGORIES:

BiologyChemistryConstructionCultureEcologyEconomyElectronicsFinanceGeographyHistoryInformaticsLawMathematicsMechanicsMedicineOtherPedagogyPhilosophyPhysicsPolicyPsychologySociologySportTourism

Use the information below to answer questions 43-49.

AP Microeconomics

Multiple Choice: Choose the best answer to each question. Each question is worth an equal amount. The honor code applies to this test.

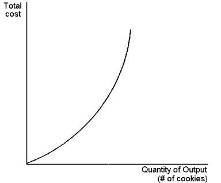

The figure below depicts a production function for a firm that produces cookies. Use the figure to answer question 1.

1. As the number of workers increases:

A. Marginal product increases, but at a decreasing rate

B. Total output increases, but at a decreasing rate

C. Marginal product increases

D. Total output decreases

2. Economies of scale occur when:

A. Long-run average total costs rise as output increases

B. Average fixed costs are falling

C. Long-run average total costs fall as output increases

D. Average fixed costs are constant

Use the information for a competitive firm in the table below to answer questions 3-7.

Quantity Total Revenue Total Cost

0 $ 0 $ 10

1 9 14

2 18 19

3 27 25

4 36 32

5 45 40

6 54 49

7 63 59

8 72 70

9 81 82

3. If this firm chooses to maximize profit it will choose a level of output where marginal cost is equal to:

A. 5

B. 7

C. 9

D. 11

4. At a production level of 3 units which of the following is true?

A. Fixed cost is zero

B. Marginal cost is $6

C. Total revenue is less than variable cost

D. Marginal revenue is less than marginal cost

5. If the firm finds that its marginal cost is $11, it should:

A. Increase production to maximize profit

B. Decrease production to maximize profit

C. Maintain its current level of production to maximize profit

D. Advertise to find additional buyers

6. At which level of production is average revenue equal to marginal cost?

A. 1

B. 3

C. 6

D. 8

7. The maximum profit available to this firm is:

A. $2

B. $3

C. $4

D. $5

8. The short-run supply curve for a firm in a perfectly competitive market:

A. Is determined by forces external to the firm

B. Is reflected in its marginal cost curve (above average variable cost)

C. Will be influenced by the magnitude of fixed costs

D. Is likely to slope downward

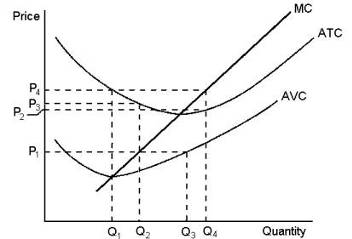

The graph below depicts the cost structure for a firm in a competitive market. Use the graph to answer questions 9-12.

9. When price falls from P3 to P1, the firm finds that

a. fixed cost is higher at a production level of Q1 than it is at Q3.

b. it is unwilling to produce any output.

c. it should produce Q1 units of output.

d. all of the above.

10. When price rises from P2 to P3, the firm finds that

a. marginal revenue exceeds marginal cost at a production level of Q2.

b. if it produces at output level Q3 it will earn zero profit.

c. expanding output to Q4 would leave the firm with losses.

d. all of the above.

11. When price rises from P3 to P4, the firm finds that

a. average revenue exceeds marginal revenue at a production level of Q4.

b. fixed costs are lower at a production level of Q4.

c. it can earn profits by increasing production to Q4.

d. profits are maximized at a production level of Q3.

12. Which of the following statements best reflects the situation faced by the firm when price falls from P4 to P2?

a. Marginal revenue is lower than marginal cost at the previous level of output, so it decreases production.

b. Marginal revenue is higher than marginal cost at the previous level of output, so it increases production.

c. Average total cost is lower than at the previous level of output so it increases production.

d. The firm will earn profit equal to (P4 - P2) x Q2.

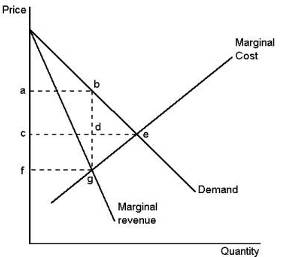

The figure below depicts the demand, marginal revenue and marginal cost curves of a profit maximizing monopolist. Use the figure to answer questions 13-14.

13. Total surplus lost due to monopoly pricing is reflected in

a. rectangle acdb.

b. rectangle cfgd.

c. triangle bde.

d. triangle bge.

14. Which of the following areas represents the deadweight loss due to monopoly pricing?

a. rectangle acdb

b. rectangle cfgd

c. triangle bde

d. triangle bge

For questions 15-18, assume that a given firm experiences decreasing marginal product of labor with the addition of each worker regardless of the current output level.

15. Average variable cost will be

a. U-shaped.

b. always rising.

c. always falling.

d. constant.

16. Average fixed cost will be

a. U-shaped.

b. always rising.

c. always falling.

d. constant.

17. Marginal cost will be

a. U-shaped.

b. always rising.

c. always falling.

d. constant.

18. Average total cost will be

a. U-shaped.

b. always rising.

c. always falling.

d. constant.

19. Diminishing marginal product causes the average variable cost curve to

a. rise.

b. fall.

c. rise until it equals the total cost curve.

d. level out.

20. Accounting profit is equal to

(i) economic profit + implicit costs.

(ii) total revenue - implicit costs.

(iii) total revenue - opportunity costs.

a. (i) only

b. (iii) only

c. (i) and (ii)

d. none of the above

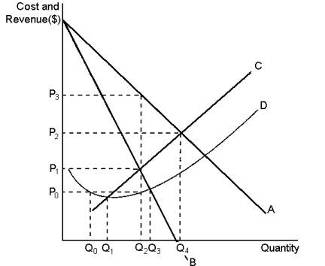

The figure below reflects the cost and revenue structure for a monopoly firm. Use it to answer questions 21-15.

21. Profit on a typical unit sold for a profit maximizing monopoly would equal

a. P3 - P2.

b. P3 - P0.

c. P2 - P1.

d. P2 - P0.

22. At the profit maximizing level of output, average revenue is equal to

a. P3.

b. P2.

c. P1.

d. P0.

23. A profit maximizing monopoly would have a total revenue equal to

a. (P3 - P0) x Q2.

b. (P3 - P0) x Q4.

c. P3 x Q2.

d. P2 x Q4.

24. A profit maximizing monopoly would have a total cost equal to

a. P0 x Q1.

b. P0 x Q2.

c. P0 x Q3.

d. (P1 - P0) x Q2.

25. A profit maximizing monopoly would have profit equal to

a. (P3 - P0) x Q2.

b. (P3 - P0) x Q4.

c. P3 x Q2.

d. P2 x Q4.

26. In order to sell more of its product, a monopolist must

a. sell to the government.

b. sell in international markets.

c. use its market power to force up the price of complementary products.

d. lower its price.

27. The efficient scale of the firm is the quantity of output that

a. maximizes marginal product.

b. minimizes average total cost.

c. minimizes average fixed cost.

d. minimizes average variable cost.

28. For a monopolist, when does marginal revenue exceed demand?

a. When output is less than profit maximizing output.

b. When output is greater than profit maximizing output.

c. When price is subject to the Law of Demand.

d. Never.

29. Marginal cost is equal to average total cost when

a. marginal cost is at its minimum.

b. average total cost is at its minimum.

c. average variable cost is falling.

d. average fixed cost is rising.

30. If marginal cost is rising

a. marginal product must be rising.

b. marginal product must be falling.

c. average variable cost must be falling.

d. average fixed cost must be rising.

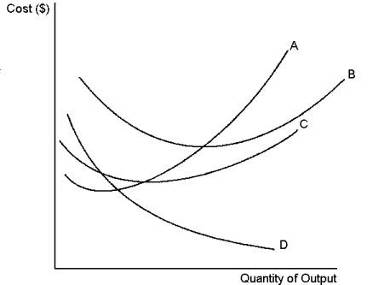

The set of lines below reflect information about the cost structure of a firm. Use the figure to answer the following question 31.

31. Line A is necessarily U-shaped because of

a. diminishing marginal product.

b. increasing marginal product.

c. the fact that decreasing marginal product follows increasing marginal product.

d. the fact that increasing marginal product follows decreasing marginal product.

Use the figures below to answer questions 32-36.

32. If the market starts in equilibrium at point C in panel (b), a decrease in demand will ultimately lead to

a. more firms in the industry, but lower levels of production for each firm.

b. a new long-run equilibrium at point D in panel (b).

c. fewer firms in the market.

d. none of the above.

33. When a firm in a competitive market, like the one depicted in panel (a), observes market price rising from P1 to P2, it is most likely the result of

a. an increase in market supply from Supply0 to Supply1.

b. an increase in market demand from Demand0 to Demand1.

c. entrance of new firms into the market.

d. the exit of existing firms in the market.

34. Assume that the market starts in equilibrium at point A in panel (b). An increase in demand from Demand0 to Demand1 will result in

a. a new market equilibrium at point D.

b. rising prices and falling profits for existing firms in the market.

c. falling prices and falling profits for existing firms in the market.

d. an eventual increase in the number of firms in the market and a new long-run equilibrium at point C.

35. When the market is in long-run equilibrium at point A in panel (b), the firm represented in panel (a) will

a. exit the market.

b. be at zero-profit equilibrium.

c. earn negative accounting profit.

d. all of the above.

36. An increase in market supply from Supply0 to Supply1 is most likely the result of

a. existing firms changing their cost structure.

b. existing firms in the market increasing their level of production beyond Q1.

c. the entrance of new firms in the market.

d. all of the above.

37. When a firm is able to put idle equipment resources to use by hiring another worker,

a. variable costs will fall.

b. variable costs will rise.

c. fixed costs will fall.

d. fixed costs and variable costs will rise.

The figure below depicts the cost structure of a firm in a competitive market. Use the figure to answer questions 38-40.

38. When market price is P2, a profit maximizing firm's losses can be represented by the area

a. (P3 - P2) x Q2.

b. (P2 - P1) x Q2.

c. At a market price of P2, the firm does not have losses.

d. At a market price of P2 the firm has losses, but the reference points in the figure don't identify the losses.

39. When market price is P5, a profit maximizing firm's profits can be represented by the area

a. (P5 - P4) x Q3.

b. P5 x Q3.

c. (P5 - P3) x Q2.

d. When market price is P5 there are no profits.

40. Firms would be encouraged to enter this market for all prices that exceed

a. P3.

b. P4.

c. P5.

d. all of the above.

41. Diminishing marginal product of labor occurs when adding another unit of labor

a. increases output, but not by as large a margin as previous units of labor.

b. decreases output.

c. increases output by more than the margin of previously employed labor.

d. none of the above.

42. Average total cost is very high when a small amount of output is produced because

a. of diminishing marginal product.

b. variable costs are spread over only a few units of output.

c. average fixed cost is large.

d. all of the above.

Use the information below to answer questions 43-49.

Measures of Cost for ABC Inc. Widget Factory

Quantity Fixed Variable Total

of Widgets Costs Costs Costs

0 $10

1 $1

2 $3 $13

3 $6 $16

4 $10

5 $25

6 $10 $21

43. The marginal cost of producing the sixth widget is

a. $1.00.

b. $3.50.

c. $6.00.

d. Cannot be determined.

44. The average total cost of producing 4 widgets is

a. $2.00.

b. $2.50.

c. $4.00.

d. $5.00.

45. The average variable cost of producing 3 widgets is

a. $2.00.

b. $3.00.

c. $3.33.

d. $5.33.

46. What is the marginal cost of producing the first widget?

a. It can't be determined from the information given.

b. $1.00

c. $10.00

d. $11.00

47. The average fixed cost of producing 5 widgets is

a. $2.00.

b. $3.00.

c. $5.00.

d. none of the above.

48. What is the variable cost of producing zero widgets?

a. $0.00

b. $1.00

c. $10.00

d. $10.00

49. What is the variable cost of producing 5 widgets?

a. $10.00

b. $15.00

c. $25.00

d. It can't be determined from the information given.

50. For a typical natural monopoly, average total cost is

a. falling and marginal cost is above average total cost.

b. rising and marginal cost is below average total cost.

c. falling and marginal cost is below average total cost.

d. rising and marginal cost is above average total cost.

51. Which of the following is a reason why a competitive firm might choose to set its price below the market price?

a. Because this would result in higher profits.

b. Because this would result in lower total costs.

c. Because this would result in higher average revenue.

d. none of the above.

Use the following information to answer questions 52-54. Adrian’s Premium Boxing Service subcontracts with a chocolate manufacturer to box premium chocolates for their mail order catalogue business. She rents a small room for $150/wk in the downtown business district that serves as her factory. She can hire workers for $275/wk.

# of workers Output Marginal Product of Labor Cost of Factory Cost of Workers Total Cost

0 0

1 330 150 275 425

2 630

3 150 825 975

4 890

5 950 60 1,375

6 10 1,800

- Adrian has received an order for 3000 boxes of chocolates for next week. If she expects that the trend in the marginal product of labor will continue in the same direction, it is most likely that her best decision will be to:

- Hire about 12 new workers and hope she can satisfy the order

- Commit to meeting the order and then take three weeks to complete the job

- Not commit to meeting the order until she can move to a larger room and hire more workers to box the chocolates

- Close her business until she is able to hire more productive workers

- What is the marginal product of the fourth worker?

a. 40

b. 110

c. 260

d. 275

- What is the total cost associated with making 890 boxes of premium chocolates per week?

a. 975

b. 1,100

c. 1,250

d. 1,375

- If a monopolist is able to perfectly price discriminate:

a. consumer surplus is increased.

b. deadweight loss is increased.

c. the price effect dominates the output effect on monopoly revenue.

d. consumer surplus and deadweight losses are transformed into monopoly profits.

56. The economic inefficiency of a monopolist can be measured by

a. the number of consumers who are unable to purchase the product because of its high price.

b. the deadweight loss.

c. the excess profit generated by monopoly firms.

d. the poor quality of service offered by monopoly firms.

57. When a firm operates under conditions of a monopoly, its price is

a. constrained by marginal cost.

b. constrained by demand.

c. constrained only by its social agenda.

d. not constrained.

58. For a profit maximizing monopolist

a. P = MR = MC.

b. P > MR > MC.

c. P > MR = MC.

d. P > MR < MC.

59. An industry is a natural monopoly when:

(i) A single firm will supply a good or service at a socially optimal quantity

(ii) A single firm can supply a fixed number of goods or services at a smaller cost than could two or more firms

(iii) A single firm can produce additional units at a smaller marginal cost

a. (i) and (ii)

b. (ii) only

c. (ii) and (iii)

d. (iii) only

The figure below depicts the cost structure of a firm in a competitive market. Use the figure to answer questions 60-62.

60. When market price is P4, a profit maximizing firm's total cost can be represented by the area

a. P4 x Q1.

b. P2 x Q4.

c. P4 x Q4.

d. Total costs cannot be determined from the information in the figure.

61. When market price is P1, a profit maximizing firm's total profit or loss can be represented by which area?

a. (P3 - P1) x Q2; loss

b. P1 x Q3; profit

c. (P2 - P1) x Q1; loss

d. We can't tell because we don't know fixed costs.

62. When market price is P1, a profit maximizing firm's total revenue can be represented by the area

a. P3 x Q2.

b. P1 x Q3.

c. P1 x Q2.

d. P2 x Q2.

63. For a firm in a perfectly competitive market the price of the good is always equal to

a. marginal revenue.

b. average revenue.

c. equilibrium market price.

d. all of the above.

64. An example of an implicit cost of production would be

a. the cost of raw materials for producing bread in a bakery.

b. the cost of a delivery truck in a business that rarely makes deliveries.

c. the income an entrepreneur could have earned working for someone else.

d. all of the above.

65. Profit is defined as

a. net revenue minus depreciation.

b. average revenue minus average total cost.

c. marginal revenue minus marginal cost.

d. total revenue minus total cost.

66. A monopoly's marginal cost will likely

a. exceed its marginal revenue.

b. equal average total cost.

c. be less than average fixed cost.

d. be less than the market price of its goods.

67. As a general rule, profit maximizing producers in a competitive market produce output at a point where

a. marginal cost is decreasing.

b. marginal revenue is increasing.

c. marginal cost is increasing.

d. price is less than marginal revenue.

68. Economic profit is equal to

a. total revenue minus the opportunity cost of producing goods and services.

b. total revenue minus the accounting cost of producing goods and services.

c. total revenue minus the explicit cost of producing goods and services.

d. average revenue minus the average cost of producing the last unit of a good or service.

69. A monopolist is a

a. price setter, and therefore has no supply curve.

b. price setter, and therefore has no variable cost curve.

c. price taker, and therefore has no supply curve.

d. price setter, and therefore has no demand curve.

70. Which of the following can eliminate the inefficiency inherent in monopoly pricing?

a. arbitrage

b. price discrimination

c. cost plus pricing

d. regulation

71. Which of the following costs do not vary with the amount of output a firm produces?

a. marginal costs and average fixed costs

b. total fixed costs

c. average fixed costs

d. total fixed costs and average fixed costs

The figure below depicts a total cost function for a firm that produces cookies. Use the figure to answer question 72.

72. The changing slope of the total cost curve reflects

a. decreasing marginal product.

b. increasing marginal product.

c. decreasing average cost.

d. increasing fixed cost.

73. Which of the following would be categorized as an opportunity cost?

(i) Wages of workers

(ii) Raw material costs

(iii) Forgone investment opportunities

a. (i) and (iii)

b. (iii) only

c. (ii) and (iii)

d. all of the above

74. In a competitive market, the actions of any single buyer or seller will:

A. Cause a noticeable change in overall production and a change in final product price

B. Have little effect on overall production but will ultimately change final product price

C. Have a negligible impact on the market price

D. Adversely affect the profitability of more than one firm in the market

75. The inefficiency of a deadweight loss stems from the fact that:

A. Consumers buy fewer units when the monopoly firm raises its price

B. High monopoly prices take money from consumers' pockets and put it in the pocket of the monopoly owners

C. Consumers who still buy the product at the high price are worse off

D. All of the above

76. A natural monopoly occurs when:

A. The monopolist product is sold in its natural state (such as water or diamonds)

B. Firms are characterized by rising marginal cost curves

C. A monopoly firm requires the use of free natural resources (such as water or air) to produce its product

D. Average total cost of production decreases as more output is produced

77. An important implicit cost of almost every business is the:

A. Cost of accounting services

B. Cost of compliance with government regulation

C. Opportunity cost of financial capital that has been invested in the business

D. Cost of debt

78. Marginal cost tells us the:

A. Marginal increment to profitability when price is constant

B. Value of all resources used in a production process

C. Amount total cost rises when output rises by one unit

D. Amount fixed cost rises when output rises by one unit

79. Because many good substitutes exist for a competitive firm, the demand curve that it faces is:

A. Perfectly inelastic

B. Perfectly elastic

C. Inelastic only over a certain region

D. Unit-elastic

80. The amount that total cost rises when the firm produces one additional unit is called:

A. Marginal cost

B. Average cost

C. Fixed cost

D. Variable cost

81. Which of the following statements best reflects a price-taking firm?

A. If the firm were to charge more than the going price, it would sell none of its goods

B. The firm has no incentive to charge less than the going price

C. The firm can sell as much as it wants at the going price

D. All of the above

82. A profit maximizing firm's short-run shut down criterion is

A. Average Revenue > Marginal Cost

B. Price < Average Variable Cost

C. Price < Average Total Cost

D. Average Revenue > Average Fixed Cost

83. If a firm produces nothing, which of the following costs will be zero?

A. Variable cost

B. Total cost

C. Average cost

D. Opportunity cost

ANSWER KEY FOR TEST

1. b. total output increases, but at a decreasing rate.

2. c. long-run average total costs fall as output increases.

3. c. 9.

4. b. Marginal cost is $6.

5. b. decrease production to maximize profit.

6. c. 6

7. d. $5.

8. b. is reflected in its marginal cost curve (above average variable cost).

9. b. it is unwilling to produce any output.

10. d. all of the above.

11. c. it can earn profits by increasing production to Q4.

12. a. Marginal revenue is lower than marginal cost at the previous level of output, so it decreases production.

13. d. triangle bge.

14. d. triangle bge

15. b. always rising.

16. c. always falling.

17. b. always rising.

18. a. U-shaped.

19. a. rise.

20. a. (i) only

21. b. P3 - P0.

22. a. P3.

23. c. P3 ð Q2.

24. b. P0 ð Q2.

25. a. (P3 - P0) ð Q2.

26. d. lower its price.

27. b. minimizes average total cost.

28. d. Never.

29. b. average total cost is at its minimum.

30. b. marginal product must be falling.

31. c. the fact that decreasing marginal product follows increasing marginal product.

32. c. fewer firms in the market.

33. b. an increase in market demand from Demand0 to Demand1.

34. d. an eventual increase in the number of firms in the market and a new long-run equilibrium at point C.

35. b. be at zero-profit equilibrium.

36. c. the entrance of new firms in the market.

37. b. variable costs will rise.

38. d. At a market price of P2 the firm has losses, but the reference points in the figure don't identify the losses.

39. a. (P5 - P4) ð Q3.

40. d. all of the above.

41. a. increases output, but not by as large a margin as previous units of labor.

42. c. average fixed cost is large.

43. c. $6.00.

44. d. $5.00.

45. a. $2.00.

46. b. $1.00

47. a. $2.00.

48. a. $0.00

49. b. $15.00

50. c. falling and marginal cost is below average total cost.

51. d. none of the above.

52. c. not commit to meeting the order until she can move to a larger room and hire more workers to box the chocolates.

53. b. 110

54. c. 1,250

55. d. consumer surplus and deadweight losses are transformed into monopoly profits.

56. b. the deadweight loss.

57. b. constrained by demand.

58. c. P > MR = MC.

59. b. (ii) only

60. b. P2 ð Q4.

61. a. (P3 - P1) ð Q2; loss

62. c. P1 ð Q2.

63. d. all of the above.

64. c. the income an entrepreneur could have earned working for someone else.

65. d. total revenue minus total cost.

66. d. be less than the market price of its goods.

67. c. marginal cost is increasing.

68. a. total revenue minus the opportunity cost of producing goods and services.

69. a. price setter, and therefore has no supply curve.

70. b. price discrimination

71. b. total fixed costs

72. a. decreasing marginal product.

73. d. all of the above

74. c. have a negligible impact on the market price.

75. a. consumers buy fewer units when the monopoly firm raises its price.

76. d. average total cost of production decreases as more output is produced.

77. c. the opportunity cost of financial capital that has been invested in the business.

78. c. the amount total cost rises when output rises by one unit.

79. b. perfectly elastic.

80. a. marginal cost.

81. d. all of the above.

82. b. Price < Average Variable Cost.

83. a. variable cost

Date: 2015-12-24; view: 2450

| <== previous page | | | next page ==> |

| LABORATORY WORK № 45 | | | Answer Key – Unit 5 |